LEHMAN, LEE & XU China Lawyers

China Banking Lawyers Alert

November 25, 2014

Attorney Edward Lehman, Managing Director of LEHMAN, LEE

& XU working 27+ years on the ground in mainland China.

Connect with Attorney Edward Lehman

![]()

|

|

|

LEHMAN, LEE & XU China Lawyers

|

|

China Banking Lawyers Alert

|

|

November 25, 2014

Attorney Edward Lehman, Managing Director of LEHMAN, LEE & XU working 27+ years on the ground in mainland China. Connect with Attorney Edward Lehman

|

The China Law News keeps you on top of business, economic and political events in the China. |

|

|

|

In the News |

Update on PRC Cross-Border Lending Transactions |

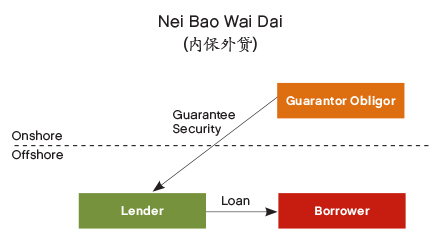

The State Administration of Foreign Exchange ("SAFE") of the People's Republic of China ("PRC") is the body that supervises the country's foreign exchange transactions. SAFE recently issued two circulars to encourage cross-border transactions: Circular No. 29 [2014] Provisions on Foreign Exchange Administration of Cross-Border Guarantee and Security (跨境担保外汇管理条例) ("Circular 29") and Circular No. 37 [2014] Issues Relating to the Administration of Foreign Exchange in Respect of Offshore Investments, Financings and Return Investments by Domestic Residents through Special Purpose Vehicles (国家外汇管理局关于境内居民通过特殊目的公司境外投融资及返程投资外汇管理有关问题的通知) ("Circular 37"). Circular 29 took effect on June 1, 2014, and Circular 37 was issued on July 14, 2014. Both support China's strategy for domestic companies to "go global" by relaxing restrictions on foreign exchange transactions. http://www.jonesday.com/update-on-prc-cross-border-lending-transactions-08-20-2014/ |

|

If you would like us to send you new issues by e-mail each month, please click here to subscribe. There is no charge for this service. If not, please click here to unsubscribe (Please provide the correct Email address which you received our message or forward the message which you received to us for further process).If you have any difficulty subscribing or unsubscribing, please contact our IT department directly at: it@lehmanlaw.com

Proud Member of

|